On 06 February 2025, the UAE Ministry of Finance and Federal Tax Authority (MoF/FTA) released a draft electronic invoicing (eInvoicing) data dictionary (PINT AE) for public consultation, based on the Peppol PINT specifications. The public consultation will last three weeks, during which time stakeholders can share feedback and help shape the disclosure requirements ahead of the 2026 reporting mandate.

In this alert, we focus on key updates, implications, and actions you can take from today to be prepared, considering what we have learnt from this publication.

What is a data dictionary?

A data dictionary is a term used to describe the “fields” needed to be submitted as part of an eInvoice. Peppol (the international framework chosen by the UAE for eInvoicing) uses a data dictionary called Peppol International Invoice (PINT).

What’s in PINT?

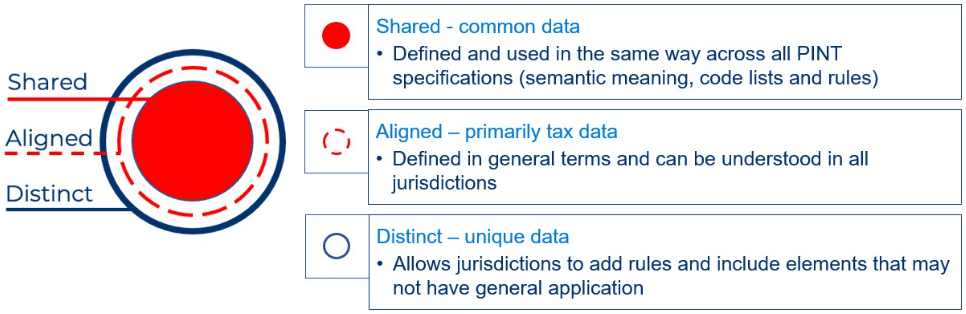

Data in PINT can broadly be categorised as falling into one of the following:

Image courtesy of Peppol from: PINT Specialization Guide, retrieved February 2025

Shared and aligned data categories of PINT allow Peppol to be interoperable across different countries that implement the framework. This makes it possible for taxpayers in one country to send eInvoices and various types of other data (e.g., procurement data) to other party in a country where Peppol has also been implemented. Drawing our attention to data considered distinct – in the UAE,

MoF/FTA have defined several data items (fields) specific to the UAE. This, together with the shared and aligned fields, form UAE’s implementation of PINT (PINT AE).

Prior to PINT, Peppol standardised data using a dictionary called Peppol BIS Billing 3.0. As the UAE is a relatively early adopter of PINT, we expect there will be updates and enhancements to the dictionary both from now until July 2026, as well as refinements and updates after Phase 1 too.

For further reading, consider reviewing Peppol’s PINT guide.

Key updates

The draft data dictionary from MoF/FTA, provides details regarding what data fields will be required across a range of invoicing scenarios (use-cases), as well as confirming some discussion points, reaffirming others, and providing greater clarity on some key areas. The two biggest areas are:

- The key data fields and their attributes for the most used invoice types by businesses in the UAE. Of note are the line-item and categorisation requirements.

- This document fleshes out some of the technical mechanisms by which messages and responses are to be sent/received between MoF/FTA and ASPs. This will be later expanded on in the infrastructure specifications.

Taxpayers will need to consider how they are going to prepare for the mandate.

Analysis

The following summarises what we believe to be the most important elements of the announcement for taxpayers, along with our perspectives:

- Tax data fields : PINT AE includes several tax fields, aligned and extending the invoice and disclosure requirements from VAT legislation. There are 15 additional data fields for tax invoices (16 for commercial invoices).

Comments : Some of the new requirements include invoice transaction classification and tax categories.There is a strong emphasis on tax. In particular, the disclosure of line-item level granularity is noteworthy; whilst this has been a longstanding requirement taxpayers fall short. Taxpayers will need to ensure transactions are captured at line-item granularity, and that tax classification is accurate when invoices are raised.

Taxpayers may find value in maintaining a reconciliation between their periodic tax returns and the eInvoices, to reduce avoidable differences and mitigate scrutiny. - Technical specifications : The document expanded on the message and response mechanism between ASPs and MoF/FTA. This includes the Tax Data Document (TDD) and Message Level Status (MLS) between ASPs and MoF/FTA. The service level (SLA) expected for ASPs to report to MoF/FTA is near real-time.

Comments : while expected, such SLAs mean ASPs will need to invest in testing and optimising their architectures to meet this requirement. MoF/FTA have clarified further that the expectation will be “minutes”, not hours or days, wide enough to allow batch processing, which will be significantly more efficient in processing over serial processing and as such, can bring down the cost per transaction.

Also note that this SLA is for the ASP, i.e., from the point at which an ASP receives an invoice. The reporting window for taxpayers to raise an eInvoice is yet to be announced; we expect this with the upcoming legislation.

- Changes to the UAE eInvoicing framework : three significant changes:

- the buyer ASP now also shares eInvoices received from the seller ASP with MoF/FTA

- the language used in publications to describe the MoF/FTA role in the model now includes validate, along with earlier drafts’ collect and store.

- MoF/FTA will be a Peppol access point.

Comments : with the buyer ASP also sharing eInvoices, MoF/FTA can check both parties received the same data. More broadly, a central data platform helps MoF/FTA achieve near real-time risk assessment and audit capability.

Taxpayers should look to develop robust data-driven validation and audit processes during implementation and consider how their choice of software supports them in achieving this.Corner 5 being a Peppol access point means that there is no special protocol for sharing data between ASPs and MoF/FTA. This can simplify the MoF/FTA integration effort needed to be taken by ASPs; taxpayers may see modest benefits.

- Use cases : MoF/FTA published a provisional list of 16 common scenarios (use-cases) for eInvoicing, along with the disclosure requirements for each.

Comments : this is an area where MoF/FTA are eager to receive feedback. We will be sharing additional scenarios which we encounter with our clients, such as advanced payments and milestone-based invoicing. We encourage all taxpayers to review the list and consider any scenarios they encounter that are not listed.

- Confirmations : Phase 1 go-live (July 2026) has been reaffirmed by MoF/FTA

Comments : the reaffirmation of the July 2026 go-live date provides certainty for both taxpayers and ASPs to plan their eInvoicing implementation and motivates all parties to move out of “wait and see” mode. We expect the phased rollout to begin on time on July 2026 – starting with the largest taxpayers.

- Imports and exports : exports by UAE taxpayers will be reported to MoF/FTA via eInvoicing. For imports, taxpayers are not required to report via eInvoicing and will continue to do so via the VAT return.

Comments : foreign sellers may choose to use Peppol to share eInvoices if they are on the network, but there is no obligation to do so. We may see this in a limited number of cases, such as a UAE importer mandating eInvoices from overseas suppliers as part of their commercial terms.For exports, there are two possible situations:- if the buyer uses Peppol (e.g., they are in a country that mandates it), the seller will include the buyer’s Peppol endpoint when issuing the invoice.

- if the buyer does not use Peppol, the seller will use a special Peppol endpoint in place of the buyer’s endpoint.

- Other areas :

- MoF/FTA have indicated in working groups their intention to mandate (currently optional) product/service codes in the future.

Comments: when HSN codes become mandatory, taxpayers will be challenged to comply. Most businesses do not maintain internationally accepted HSN codes. Taxpayers will need to undertake a mapping activity from inventory to HSN codes and build capability to maintain this. This challenge will be particularly felt by taxpayers with high variety, high volume or high value transactions. Whilst tax determination engines can be valuable here in facilitating accurate tax classification at the point of transaction, more immediate value will come from a review of the data in various systems to ensure it is complete, correct and up to date. - No new data storage or data residency requirements

Comments: this helps taxpayers avoid incurring any additional costs on data storage requirements. In addition, taxpayers are not constrained to choosing vendors based on local hosting, unless such a requirement is dictated by legal obligations or specific organisational policies. - MoF/FTA will not mandate or provide a standard protocol for communications between taxpayer systems and ASPs

Comments: the risk of vendor lock-in through prohibitive switching costs (particularly from esoteric implementation protocols) can be acute. Taxpayers should select their ASP vendor carefully, considering a breadth of perspectives and requirements – such as interoperability, scalability, compliance support, data security and business value. - No requirement for a QR code on physical or digital invoices

Comments: whilst QR codes can help buyers and other stakeholders authenticate and validate invoices, such a feature is best suited to regimes in which invoices are cleared by the tax authority – unlike the UAE. In this vein, it remains to be seen what – if any – digital signature requirements will be mandated to support verification.

- MoF/FTA have indicated in working groups their intention to mandate (currently optional) product/service codes in the future.

Moving forward

This is an exciting development in the eInvoicing implementation journey here in the UAE. Taxpayers, big and small, can begin preparation for the eInvoicing mandate. Now is the right time to be laying the groundwork for a smooth and value-adding implementation.

Consider participating in the public consultation process by reviewing the data dictionary against your own invoicing scenarios. The feedback window remains open until 27 February 2025.