Introduction

On 24 October 2024, the UAE Ministry of Finance (MoF) officially announced implementation of Electronic Invoicing (eInvoicing) in 2026 in line with its goal to build a digital economy. This initiative aims to simplify invoicing, promote digital transformation, and streamline tax compliance processes.

In this alert, we focus on key updates, implications, and actions to be taken ahead of time.

Key Updates

The material, published on the new MoF eInvoicing resource portal, confirms several previously decisions and details, while providing clarity on other important areas including:

- Filing and other technical mechanisms

- Key dates and timelines

- Scope and phasing

Confirmations

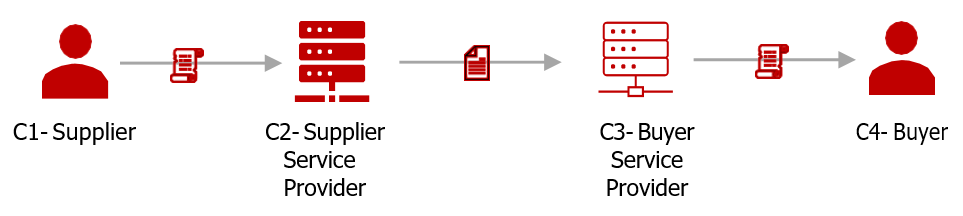

Model: MoF confirmed that they will be implementing the Decentralised Continuous Transaction Control and Exchange (DCTCE) / Peppol 5-Corner model using PINT as the data dictionary.

Timelines:

- Q4 2024: Accreditation for Service Providers & procedures

- Q2 2025: Relevant legislation updates

- Q2 2026: Phase 1 go-live for eInvoicing implementation

Analysis

Focusing on what we believe to be the most important parts of the announcement, the following summarises those details along with our perspectives on its relevance for taxpayers in the UAE:

- Data dictionary: The UAE has confirmed the use of Peppol International (PINT) as the UAE eInvoicing data dictionary.

Comments: Whilst expected, this confirms that the UAE will implement same data model as many other countries, bringing the benefits of being interoperable – making it easier for organisations to exchange invoices with many of their counterparties overseas. - Phased implementation: The mandatory rollout will be conducted in phases, with businesses implementing at stages according to criteria yet to be announced.

Comments: This is a welcome clarification. Adopting a phased approach will help reduce challenges typically faced by taxpayers and authorities during such rollouts., which can include infrastructure and software teething issues, resource and talent constraints, and taxpayer readiness.

Organisations should monitor announcements regarding the phases; some will have more time than others to prepare and implement the necessary changes. - Scope: The mandate will apply to all business transactions (B2B), including those involving non-VAT registered entities and transactions with government entities (B2G).

Comments: The inclusion of non-VAT registered entities is particularly significant for SMEs. Ahead of the mandate phase applying to them, such organisations will need to obtain a TIN from the FTA, even if they do not need to file a VAT return.

We await details of the support (if any) that will be provided to SMEs to help comply with the eInvoicing mandate. We have seen this take the form of a provision for a limited volume of free or discounted invoices. Notwithstanding this potential support, SMEs will need to consider the suitability of their current billing and payment processes. - Format: Only XML-format eInvoices will be compliant, excluding formats like PDFs and images.

Comments: This helps with an oft-misunderstood detail. Whilst some countries accept a humanreadable PDF document with machine-readable XML embedded, what is required to be produced and preserved in the UAE is only the XML. Organisations should ensure they consult with their ASP about how they will support the presentation of eInvoice data for a host of governance and control processes where the XML would be impractical to work with. - Reporting time: A near real time integration between businesses and UAE ASPs.

Comments: Together with (yet to be announced)reporting regulations, this can have significant process implications for organisations where raising invoices may currently be slow or error-prone. These organisations will need to face the challenge of issuing invoices that are complete, correct, and timely – as an invoice will be received by the MoF/FTA in the same form, with the same details, and at the same time it is issued. - Internally-developing an eInvoicing solution: A business can develop its own eInvoicing solution if they register as an ASP adhering to the UAE accreditation procedures.

Comments: With the imminent release of the first list of Accredited Service Providers (ASPs), organisations need to evaluate whether it is viable to self-develop eInvoicing technology, which includes maintaining compliance with changing regulations and maintaining an SLA for the broader exchange.

Between the options of using an ASP or building a home-grown solution, some vendors are offering organisations a middle path – to license their software for self-hosting. While this can reduce development costs, organisations considering this will still need to separately register as an ASP and meet their commitments on the exchange. - VAT groups: Each member of the VAT group must have an endpoint via a UAE Accredited Service Provider. The endpoint refers to identification of the member entity. When issuing an invoice, the group’s Tax Registration Number (TRN) should be provided, but the endpoint details should correspond to the specific group member conducting the transaction.

Comments: Despite having the same TRN and a single tax filing for VAT groups, each member company will need to maintain its own unique “address” for receiving invoices with their ASP, which may have cost implications. Organisations will also likely need to work with their customers to update their master data in preparation for eInvoicing. - Tax invoice errors: In case of any errors in tax invoices, a credit note is required to be issued for its rectification.

Comments: While some implementations allow for a grace period to correct an invoice without issuing a credit note, this is not the intention in the UAE.

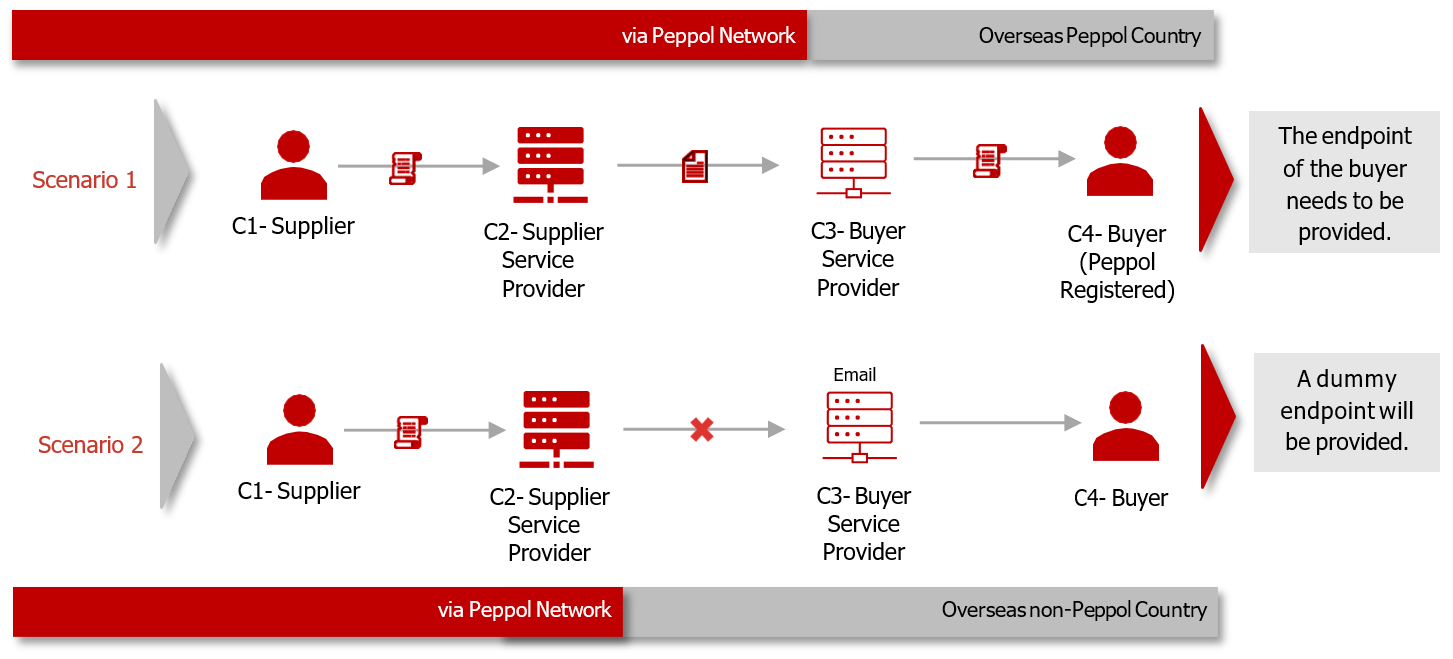

Organisations, especially highly transactional businesses, should review their reconciliation and reporting processes, such as VAT compliance. - Exports: When the seller initiates a transaction with a foreign buyer there could be two possibilities – the buyer may or may not be registered within the Peppol network.

Comments: Let us understand this through a diagram:

- Imports/self-billing: Organisations will be able to receive eInvoices from other Peppolimplementing countries, should they want to.

Comments: In certain situations, the recipient business may be required to issue a tax invoice themselves – for example, in cases of imports or when there is an agreement with the seller to issue a buyer-created tax invoice. Such invoices will also need to be reported to the FTA using the eInvoicing mechanism. - Interface between taxpayers and ASPs: Typically, the interface would be based on Application Program Interfaces (APIs), web interfaces, or SFTP/ETL methods.

Comments: When selecting an ASP vendor, organisations should match what their business systems can support (both ways) with what the vendor ASP can offer, as the format and mechanisms involved in this leg of the document exchange depends on both parties. Encryption can also differ, impacting data security and integrity.

Tangentially, organisations should take the time to critically evaluate a vendor ASP’s format requirements, as esoteric configurations can lead to lock-in with the vendor or expensive future reimplementations.

Moving forward

In light of this recent announcement from the MoF, we recommend organisations big and small consider the following as they prepare for the eInvoicing mandate:

- Conduct discovery and documentation: Ensure your current systems, processes, and data can accommodate the introduction of eInvoicing. Pay particular attention to data quality, especially master data, as this is a common area needing improvement.

- Build awareness: Foster awareness of eInvoicing within your organisation to ensure the right level of commitment and establish a working group to manage significant process changes, particularly for highly transactional organisations.

- Engage with prospective ASPs: Start conversations with potential Accredited Service Providers (ASPs) to understand the available options and their implications.

- Define success: Develop a clear vision of what a successful implementation will achieve. Success can range from regulatory compliance to driving efficiencies in invoice processing and tax return preparation, as well as leveraging transactional data for better business insights.