The Zakat, Tax and Customs Authority (ZATCA) in Saudi Arabia has introduced the Advanced Pricing Agreement (APA) mechanism by virtue of its Transfer Pricing Bylaws and the APA Guidelines.

In Part I of the APA Series, we discussed the key features of the APA mechanism and in Part II, we elaborated on the process of making the APA application highlighting the practical challenges arising in the process.

As we culminate the APA Series in Part III, we discuss the possible outcomes of an APA application i.e the scenarios where the application is rejected or subsequently revoked by ZATCA. We also discuss certain areas in which ZATCA wish to issues clarification to enhance transparency and clarity in the APA process.

Let’s read on to find out more!

Different Outcomes of APA Application

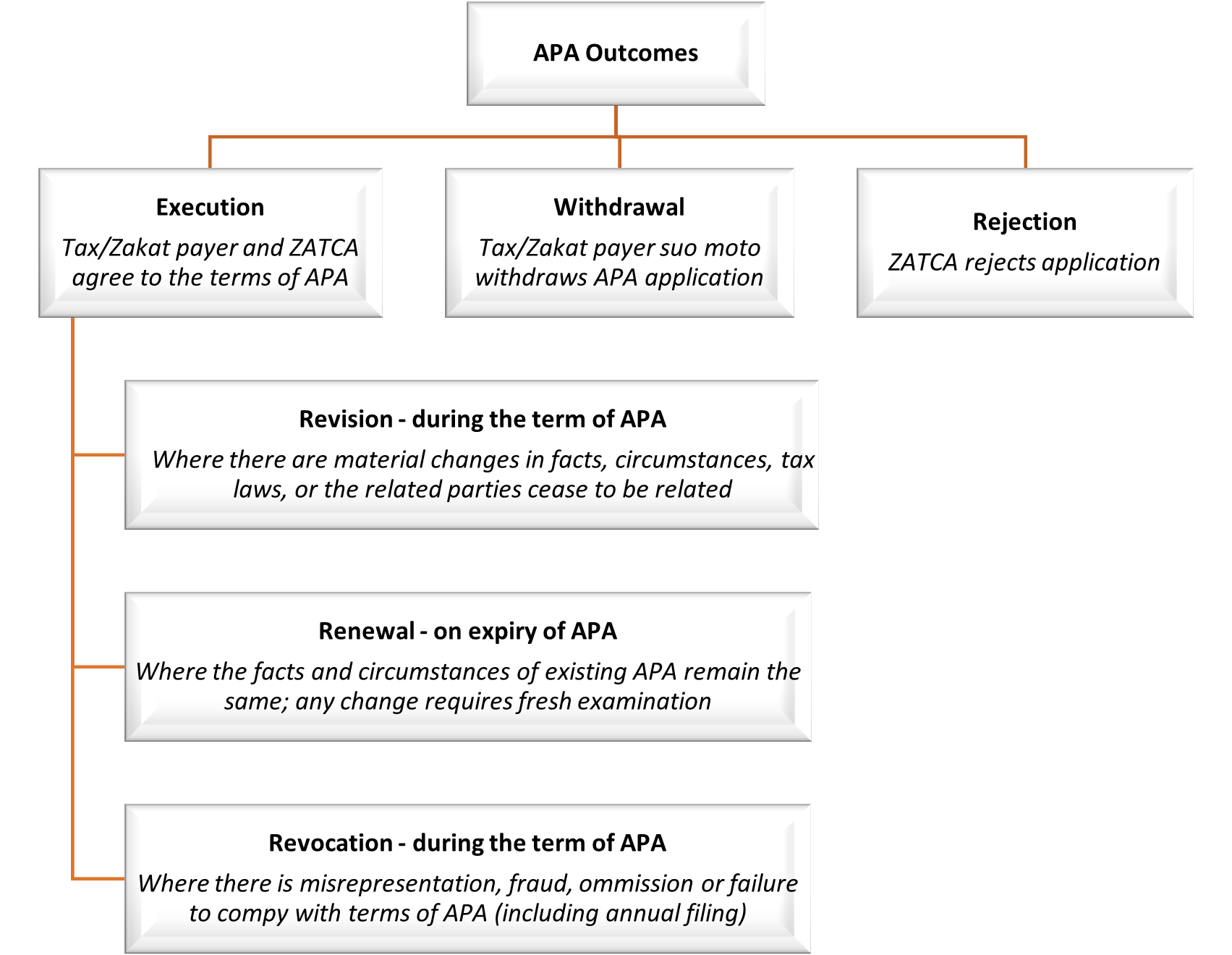

An APA may be formally executed between ZATCA and the Tax/Zakat payer. Alternatively, the application may be rejected or revoked by ZATCA, or voluntarily withdrawn by the Tax/Zakat payer. The regime also provides flexibility for revising or renewing an APA once it has been executed. The graph below gives a bird’s eye view of the possible APA outcomes.

While the above graph is self-explanatory, there are some aspects which require attention as discussed further in this part of the APA Series.

Rejection of the APA Application

The ZATCA may reject the APA application at any point in time during the application process. Some of the reasons for rejection include:

- unreasonable delays or failure to provide complete and accurate information by the Tax/Zakat payer;

- non-adherence to the arm’s length principle (ALP) in transactions with related parties;

- inability to evaluate the correct application of ALP (eg. in case of complicated transactions like e-commerce business models sans physical nexus, sharing intra-group expenses in crypto assets and related businesses etc.);

- transactions being hypothetical;

- possibility of tax evasion or tax avoidance;

- significant transformation or change in circumstances during the APA period; or

- failure of the parties to arrive at agreeable terms of APA.

The risk of rejection can be mitigated by way of a well-drafted application and an appropriate presentation of the facts and transfer pricing methods (TPM) at the time of meeting with the ZATCA.

The Guide provides that the ZATCA has the discretion to notify the reasons of rejection to the Tax/Zakat payer. Further, although the Tax/Zakat payer may respond to the rejection notice within 30 days, the ZATCA’s decision will be final. However, certain procedural gaps remain in the rejection process. To ensure fairness and alignment with international best practices, the ZATCA may consider the following enhancements to the Guide:

- Right to be heard: Where the ZATCA intends to reject an APA application, the Tax/Zakat payer should be granted an opportunity to present their case, clarify technical positions, and respond to any concerns raised by it.

- Reasonable response period: Upon issuance of a rejection notice, the Tax/Zakat payer must be provided a reasonable timeframe (say 30 days) to submit written objections or supplementary documentation before the rejection is finalized.

Revision of the Executed APA

An executed APA may be revised if there is a material change in the facts and circumstances, i.e change of the Zakat / Tax law or the nature of relation between the transacting related parties. For instance, in case of a merger between the related parties, where one party ceases to exist, the existing APA must also cease to exist. Likewise, if a related party in hived off and ceases to be part of the group, the APA may be revised to the extent there is change in the facts / circumstances of the agreed critical terms and conditions.

The Guide casts a responsibility on the Tax/Zakat payer to inform the ZATCA about any such change so that the APA can be revised.

There are no defined timelines governing key aspects of the APA revision process. Specifically, there is no clarity on when the Tax/Zakat payer must notify the ZATCA about a change that requires revision, when the ZATCA should initiate the revision procedure, or by when the revision must be completed. Hence, it is important for the Tax/Zakat payer as well as their transfer pricing advisor to be proactive and inform the ZATCA about any change in the facts and circumstances that may warrant a revision of the executed APA.

Revocation of the APA

The Guide states that the ZATCA may revoke an executed APA at any time during its term in cases of misrepresentation, mistake, fraud, or omission in the Tax/Zakat payer’s submissions; failure to comply with material terms of the APA; or delayed filing of the Annual Compliance Report (ACR).

Revocation of the APA is initiated by the ZATCA. Needless to say, the ZATCA must have sufficient evidence to prove that the APA deserves a revocation.

Upon revocation, the APA is either deemed ineffective from the start or for the rest of part of the specified period in the APA as may be directed by ZATCA. While the ZATCA is required to notify the Tax/Zakat payer of the reasons for revocation, the process does not provide the Tax/Zakat payer an opportunity to be heard or to respond before the APA is revoked. Further, any revocation must be reviewed by senior officials in the ZATCA before a communication is issued to the Tax/Zakat payer. The lack of procedural fairness in the Guide may warrant reconsideration.

Renewal of the APA

Renewal requests must be submitted at least 12 months before the start of the new fiscal year and generally follow the same process as the initial APA application. The ZATCA may approve renewal under similar terms if the TPM remains effective, critical assumptions are unchanged, and the Tax/Zakat payer has demonstrated full compliance. However, if there are material changes in facts, business models, or industry conditions, the Tax/Zakat payer must propose amendments supported by updated analysis and documentation.

For instance, a fintech firm operating in the KSA had an APA covering its intra-group software licensing arrangements. Over the APA term, the firm expanded into AI-driven analytics, altering its revenue model and cost structure. For renewal, the Tax/Zakat payer must submit revised benchmarking analysis to renew the APA with modified terms.

Compliance with the terms of APA

Once an APA is executed, the Tax/Zakat payer is bound by the terms, conditions, and critical assumptions set out in the agreement. It may require the Tax/Zakat payer to make certain corresponding adjustments to arrive at ALP. Further, annual compliance filings and proper documentation are mandatory. If the Tax/Zakat payer fails to meet these conditions, the continuation of the APA is in jeopardy.

Let’s understand with the help of an example.

A Tax/Zakat payer, CryptoBridge, entered into an APA with ZATCA covering its intra‑group services. However, during subsequent years, the company’s Zakat/Tax filings deviated from the APA’s agreed‑upon covered transactions and pricing terms. CryptoBridge unilaterally reclassified certain services, altered margins, and failed to notify ZATCA of these changes or update the supporting documentation. Due to these discrepancies and poor record-keeping, the APA was revoked.

This example underscores the critical need for consistent alignment between APA terms and actual filings, timely communication with the authority regarding any changes in facts or assumptions, and robust documentation practices to support ongoing compliance.

Conclusion

The APA framework in Saudi Arabia offers valuable certainty, but procedural gaps especially around rejection, revision, and revocation can undermine Tax/Zakat payer confidence. Strengthening the Guide with defined timelines, the right to be heard, and transparent review mechanisms would enhance fairness and predictability.

It is pertinent to note that the APA mechanism is an initiative for the benefit of the Tax/Zakat payers. It casts a huge responsibility on the them to provide correct facts, adhere to the terms of the APA, make regular compliances and proactively inform the ZATCA about any change in fact or material assumptions. This is a joint effort between the Tax/Zakat payers and their advisors.

Author

Gopal Agarwal

Director